Roadtrip Dirtbag Finance

18 Jul 2019 - Michelle Ho

This post includes math (!)

How much did our road-trip cost us? That depends, of course. Are we including opportunity cost of leaving our jobs? Are we deducting normal living expenses (like groceries, housing, restaurants) that we would’ve spent if we’d stayed in NYC to see how much it marginally cost (or saved) us to go on the road-trip? It can get complicated.

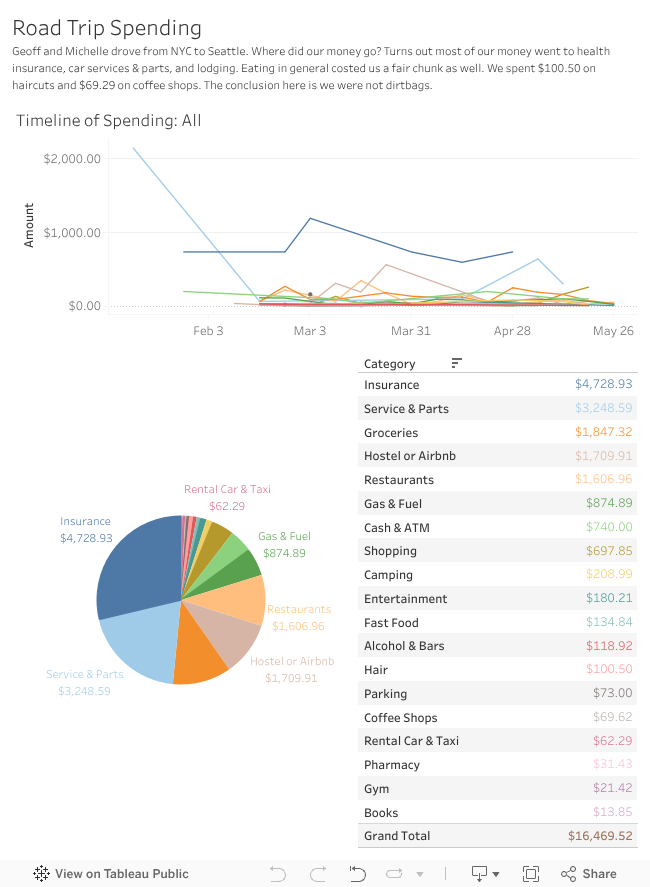

I decided to look at all the transactions that Geoff and I accumulated pertaining to the road-trip. I also included things like upgrades we got to the car beforehand and health insurance, which significantly increased our spending total. Both Geoff and I track our money via Mint, so it was just a matter of downloading all our transactions, putting them together in one spreadsheet, spotfixes for certain categories, and then creating the visualization with Tableau. Our grand total? $16,469.52. Spoiler: we are not dirtbags.

Let’s do some math

But let’s revisit the idea of opportunity costs! Geoff and I talked about this while on the road. We boiled down opportunity cost to two competing forces: rate of salary increase and interest rate.

Let’s say, for example, you’re fresh out of school, haven’t started working yet, and are trying to decide between taking a gap year off now versus in 9 years.

Case 1 (no interest rate, no salary increase)

If you expect your salary to stay the same over time and we ignore the existence of interest, then there’s no difference when you take your time off. The opportunity cost is the same.

Case 2 (only salary increase)

If you expect to be making more later in life, then taking time off now is better. The opportunity cost later in life will be higher.

Case 3 (only interest rate)

If you consider an interest rate, the opportunity cost of taking a year off will be higher now, assuming your salary stays the same.

Now for a Math Problem!

Let’s assume your starting salary is $50,000 no matter when you start working. If the interest rate is 2%, what does your annually salary increase need to be in order to make no difference in 10 years from now whether you take your gap year now or in 9 years? Let’s assume that interest compounds monthly and your salary increase compounds once annually. Let’s also assume, for simplicity, you get the salary upfront at the start of every year (so you start accumulating interest on your savings right away) and you always save the same portion of your salary every year and spend all the rest of it.

The general compounding formula is:

$A = P(1 + \frac{r}{n})^{nt}$

P: Principal

r: Interest rate

t: Number of years compounded

n: Number of times interest is compounded per year

Answer:

2.01844% (rounded)

Solve this equation for b

$50000(1+\frac{0.02}{12})^{12\times10} = 50000(1 + b)^{9}(1 + \frac{0.02}{12})^{12}$

Plug back in and check:

After 9 years time, your salary will be (see right-hand side of equation above):

$50000(1+.0201844)^9 = 59851.92$

Taking a year off in 9 years time will cost you $59851.92 that you would’ve made in your 10th year plus interest in that last year, which comes out to $61060.00 (rounded to the closest cent).

The left-hand side of the equation comes out to $61059.97.

The way I’ve framed this problem, we’re finding out how much “faster” something with a monthly compounding rate grows compared to an annually compounding rate. Now, we’ve simplified this problem a lot with some unrealistic assumptions (that we get paid upfront every year, that our savings fraction remains the same, that we’re only taking one year off, that we can pay for a year off now without needing to take a loan out…) but this paints a pretty good picture. I’ll leave it as an exercise for the reader to figure out the same problem with different assumptions.

Last I checked, the average annual raise in 2019 was 3.1% and the federal benchmark interest rate was 2.25% - 2.5%. Of course, you’re probably getting different return rates (my savings account was giving me 2.10% APY) depending on what interest-bearing accounts you’re using and other investments you might have. I think my average annual raises from the last 5 years have been significantly higher than 3.1%. Take-away story: if you’re saving up to take some time off at some undetermined future date when you feel more secure, maybe it’s better to do it sooner than you think. It will be harder to take time off when you’re making more money than before, not to mention the additional life responsibilities.

Back in 2015, I wrote to pro-climber Steph Davis, asking about details of her personal financial plan. To my amazement, she actually answered me in this really long, thorough blog post: Dirtbag Financial Plan. If you enjoyed this post, then I recommend you read it!

Side note: in my letter to Steph, I complained of having a “soul-crushing office job”. I was immediately put in my place by someone in the comments section (Yes! Someone was actually right in the comments section!) by gently telling me “All work is sacred” and “You know what’s soul crushing – not having a job at all”. I concede the point, and regret describing my previous job as “soul-crushing” when it, in fact, was not. If anything, it was character-building and I look back proudly and fondly on it :)